"It's too expensive"

Let your winners ride.

Many times when people describe stocks of large companies like Amazon, Apple and Microsoft, they tell me “it’s too expensive”. I’m not immune from it - I sold some Amazon stock I owned in 2013 at $226 because I thought the same and even wrote about it. At the time, AWS was a $1.5B business (which I ended up working for) and is now close to $50B.

Fast-growing companies are ‘expensive’ for good reason. They compound revenue pretty darn quickly.

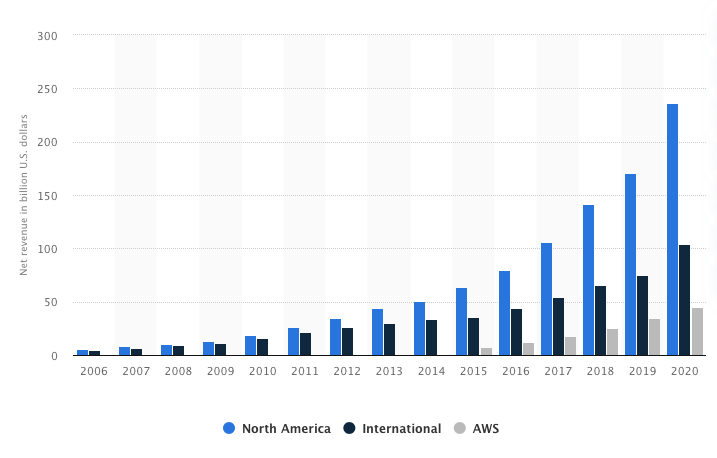

Today, Amazon announced 2021 Q1 earnings with growth of 44% year-over-year (YoY). In the last 12 months, Amazon’s revenue has surpassed $400B. They have three highly-successful segments that continue to grow exponentially.

AWS: 32% YoY

North American Retail: 50% YoY

International Retail: 60% YoY

But Safeer - it’s too expensive.

Cloud computing (AWS) and e-commerce (retail) are still in the early innings. Both segments have captured less than 20% of their respective market (IT infrastructure and general retail). These business segments will continue to thrive in the next coming decades.

On average, Amazon has been growing 30-45% year-over-year (YoY) in revenue for several years. If they continue growing at ~35% YoY, their revenue will 3x in four years.

Do the math: 1.35^4 years = 3.32.

At similar valuations and sustained growth, Amazon stock will triple in four years.

6 yr ago: $430

3 yr ago: $1400 (4x)

Today: $3500 (2.5x)

In 4 yrs: $10K (3x)

“Our favorite holding period is forever” - Warren Buffett

I buy every week.